Commercial Real Estate Crisis: Economic Implications Revealed

The current commercial real estate crisis has raised alarms among financial experts regarding its potential fallout in the coming years. With office vacancy rates skyrocketing in urban areas post-pandemic, many buildings are struggling with unusually high vacancies, some reaching up to 23%. This decline in demand has undeniably affected property valuations, stirring concerns about the broader economic impact of the real estate sector. Adding to the unease, the significant amount of commercial mortgage debt due for repayment by 2025 has prompted fears of possible bank failures, particularly among smaller institutions. As interest rates continue to influence borrowing costs, the stability of the financial system hangs in the balance, making it imperative to closely monitor these developments.

In exploring the pressing challenges within the commercial property market, it’s evident that the landscape is significantly altered by high office occupancy rates and a notable decline in real estate demand since the pandemic’s onset. This downturn in commercial space utilization poses a risk to the financial framework, impacting economic stability and igniting fears of looming bank collapses due to maturing debts. As interest rates fluctuate, their influence looms large over investment decisions, further complicating the situation for property owners burdened with loans. The intricate dynamics between economic factors and the commercial real estate market underscore a complex narrative where potential fallout could ripple beyond mere market confines, affecting various sectors intertwined with financial health.

Understanding the Commercial Real Estate Crisis

The current commercial real estate crisis stems from a combination of high office vacancy rates and rising interest rates that have put immense pressure on the sector. As of mid-2024, office vacancy rates in major U.S. cities range significantly, with figures between 12% and 23%. This decline can primarily be attributed to the shift towards remote work, which was accelerated by the pandemic. Decreased demand for office space has led to falling property values, creating a ripple effect across financial institutions that heavily invested in commercial real estate. As a consequence, many investors now face the harsh reality of having properties that are selling for about half of their original purchase price, posing significant challenges for their portfolios and the banking system at large.

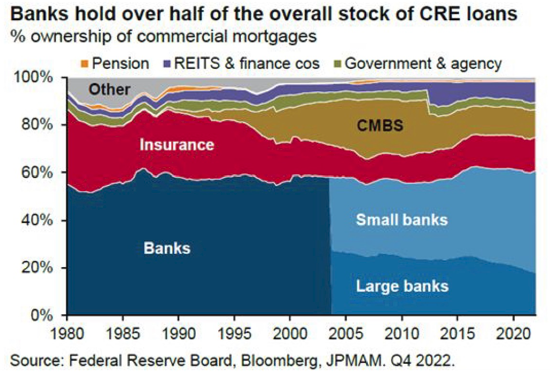

Furthermore, the looming deadline of 20% of the $4.7 trillion commercial mortgage debt set to mature this year has stirred anxiety among market analysts. If significant delinquencies occur, banks may contend with unexpected losses, further destabilizing the market. This scenario poses a question: how will financial institutions navigate the potential wave of defaults? Experts like Kenneth Rogoff suggest that while some regional banks may struggle, major banks are better positioned due to stricter regulations implemented after the 2008 financial crisis. However, the risk of a broader economic impact remains, indicating that addressing the uncertainties surrounding commercial real estate is crucial for financial stability.

The Economic Impact of High Office Vacancy Rates

High office vacancy rates can have far-reaching consequences on the economy. With businesses downsizing their physical spaces and opting for hybrid work models, the economic activity in urban centers has diminished. This trend not only affects property values but also reduces revenue for municipalities dependent on property taxes and related income from businesses. As vacancy rates soar, businesses that rely on foot traffic, such as restaurants and retail stores, are also likely to feel the pinch, potentially leading to job losses and lower consumer spending. Lowering occupancy rates contribute to economic stagnation, making it vital for communities to seek adaptive strategies that support economic revitalization in the face of changing work environments.

Moreover, the economic ramifications extend beyond immediate financial losses. As regional banks that are deeply invested in commercial real estate struggle with potential defaults, they may tighten lending standards, which can hamper access to credit for consumers and small businesses. This tightening can lower overall economic growth as businesses find it increasingly challenging to finance expansions or maintain operations. Importantly, the broader economy is experiencing a paradox where segments like the stock market exhibit significant gains, contrasting with declining real estate values, suggesting that the effects of high vacancy rates may not be uniform across all sectors.

Interest Rates and Their Influence on the Commercial Real Estate Market

Interest rates play a critical role in shaping the commercial real estate landscape, particularly as they impact borrowing costs for investors and developers. When interest rates rise, financing becomes more expensive, which can deter investment in commercial properties and exacerbate existing vacancy problems. The Federal Reserve’s recent reluctance to lower interest rates, even amidst a burgeoning crisis in commercial real estate, has left many property owners in a precarious situation. For investors who anticipated continued low rates, the sharp rise has resulted in higher financing costs and, consequently, a decline in property values due to increased capitalization rates.

Additionally, higher interest rates can lead to a feedback loop, adversely affecting financial stability. As property values drop, lenders may face increasing risk related to their exposure in commercial funding. Should delinquencies rise among properties financed at lower interest rates, banks, particularly smaller regional ones, could face significant challenges. While large banks appear sufficiently diversified to manage these risks, the strain on smaller institutions necessitates close monitoring, as any instability could amplify the commercial real estate crisis and lead to broader economic consequences.

Potential Consequences of Bank Failures on the Real Estate Sector

The potential for bank failures due to the commercial real estate crisis raises concerns regarding financial stability and economic resilience. As regional banks heavily invested in commercial properties begin to experience increased pressure from rising delinquency rates, their ability to lend could tighten, prompting a downward spiral. The ramifications of even a single regional bank failure could have a ripple effect throughout local economies, influencing credit availability for businesses and consumers alike. Banks are interconnected in the marketplace, and a failure might lead to loss of confidence that triggers further instability across the financial system.

Moreover, if small and medium-sized banks fail as a result of significant losses in their commercial real estate portfolios, many communities may suffer from reduced lending capacity. This can result in fewer resources for small businesses, stymying local economic growth, which is particularly concerning in a landscape where many firms are still recovering from pandemic-related setbacks. Therefore, addressing the vulnerabilities in regional banks should be a priority to mitigate cascading effects and maintain consumer confidence in the financial system.

Adapting to New Demand in Commercial Real Estate

As the commercial real estate landscape shifts, adapting to new demand dynamics becomes essential for both investors and policymakers. The rise in remote work has challenged traditional office space utilization, prompting a reconsideration of how commercial properties can meet modern needs. Some new strategies include transforming underutilized office spaces into mixed-use developments or incorporating flexible work arrangements into existing buildings. Stakeholders must explore innovative solutions that align commercial environments with current workforce preferences while addressing high vacancy rates that hinder economic progress.

Moreover, the demand for properties with modern amenities, like improved air quality and wellness-focused designs, is increasing as tenants seek healthier workspaces. These developments could mitigate some economic downward pressure while attracting new businesses seeking spaces that provide enhanced productivity and comfort. Policymakers may also explore incentives for converting vacant office spaces into residential units to alleviate housing shortages, demonstrating a dual approach that addresses both commercial challenges and housing needs.

The Role of Government Intervention in Real Estate Recovery

Government intervention may serve as a catalyst for recovery in the commercial real estate sector amid rising bank fears and high vacancy rates. Policies aimed at stabilizing or incentivizing lending can help mitigate the risks faced by regional banks and investors. For instance, measures that encourage refinancing options or offer financial support for commercial property owners who are struggling could alleviate some pressure on the system and prevent a cascade of defaults. A holistic approach involving both fiscal and monetary policy may enhance economic resilience while addressing the urgent needs of stakeholders across the real estate sector.

Additionally, developing frameworks that promote sustainable growth in the real estate market can enhance long-term stability. This might include incentives for green building practices or the adoption of technology in property management. By aligning economic goals with environmentally responsible strategies, governments can foster a more resilient and adaptive real estate sector that supports both local economies and the broader market.

Financial Stability Amid Commercial Real Estate Challenges

Maintaining financial stability amidst the commercial real estate turmoil is paramount for both economic growth and consumer confidence. The interplay between high vacancy rates, rising interest rates, and potential bank failures creates a complex environment that requires careful navigation. Financial experts argue that while the potential for widespread bank failures exists, the large banks that emerged from the 2008 crisis are better equipped to handle such shocks due to increased regulatory oversight. Such dynamics underscore the importance of vigilant risk management practices as the market adjusts.

Furthermore, fostering transparency within the banking sector and among investors can promote resilience as stakeholders assess their exposure to commercial real estate. An informed market can better withstand fluctuations and recover from downturns, ultimately supporting overall economic vitality. Ensuring that consumers remain aware of the implications of financial changes on real estate, alongside proactive policy measures, will be essential to sustaining confidence in both the banking system and the broader economy.

Future Outlook for Commercial Real Estate

The future outlook for commercial real estate is currently clouded with uncertainty, as stakeholders grapple with evolving market dynamics shaped by pandemic-related workforce changes and financial factors. While there are significant challenges, including the anticipated wave of loan maturities and the high levels of office vacancy rates, there are also opportunities for innovation and adaptation. The resilience demonstrated by various segments of the market, such as logistics and warehousing, reflects a shift towards more sustainable and demand-responsive real estate practices.

Looking ahead, the real estate sector must leverage technology to improve operational efficiencies and address shortcomings exposed during the pandemic. Stakeholders should prioritize flexible leasing arrangements, mixed-use developments, and sustainability-focused initiatives that respond to changing consumer preferences. By fostering an adaptive environment within commercial real estate, the industry can emerge from its current crisis stronger and better aligned with future economic realities.

Mitigating Risks Associated with Commercial Real Estate Investments

Mitigating risks tied to commercial real estate investments will require a multifaceted strategy that spans market analysis, deploying innovative financial instruments, and ensuring robust risk assessment frameworks. Investors should focus on diversification across property types and geographical markets to cushion against localized downturns. Understanding particular market trends and consumer behavior is integral in retaining asset value and ensuring long-term profitability, especially in an environment characterized by volatile interest rates and shifting demand.

Moreover, developing strong partnerships with financial experts can provide investors with insights needed to navigate the complex landscape of commercial real estate. Engaging in proactive risk management practices, including analyzing debt structures and potential market shifts, will be critical for safeguarding asset portfolios. By taking a holistic approach to mitigating risks in commercial real estate investments, stakeholders can enhance the resilience of their strategies and contribute positively to the overall economic landscape.

Frequently Asked Questions

How are high office vacancy rates contributing to the commercial real estate crisis?

High office vacancy rates, particularly those hovering around 12 to 23 percent in major U.S. cities, are significantly driving down property values, which worsens the commercial real estate crisis. This decline in demand for office space, partly due to shifts in work habits post-pandemic, creates financial strain on property owners and investors, negatively impacting the overall economy.

What is the potential economic impact of the commercial real estate crisis on banks?

The commercial real estate crisis poses a threat to banks, particularly regional ones that hold substantial amounts of commercial real estate loans. If significant delinquencies occur as many loans come due, this could lead to increased vulnerabilities in these banks, potentially resulting in losses and financial instability across the banking sector.

How might current interest rates influence the commercial real estate crisis?

Current high interest rates exacerbate the commercial real estate crisis by making refinancing more difficult for property owners. Many commercial properties are over-leveraged, and as interest rates remain elevated, the cost of borrowing increases, leading to potential defaults and additional pressures on the financial stability of banks and investors.

Could economic downturns lead to further deterioration in the commercial real estate market?

Yes, significant economic downturns could amplify the commercial real estate crisis. A recession would likely increase unemployment and reduce business investment, consequently driving up office vacancy rates and creating a domino effect of financial difficulties, particularly for banks heavily invested in commercial real estate.

What role do bank failures play in the commercial real estate crisis?

Bank failures could significantly impact the commercial real estate crisis by limiting access to capital and creating tighter lending conditions. As regional banks face losses from bad real estate loans, they may reduce lending, further hampering investment in commercial properties and exacerbating the crisis.

Are there any strategies to mitigate the impacts of the commercial real estate crisis?

Mitigating the impacts of the commercial real estate crisis may involve government interventions, such as providing financial support to banks facing losses or creating incentives to convert unoccupied office buildings into residential units. However, long-term solutions require addressing underlying issues, such as adjusting interest rates or initiating economic recovery measures.

How has the pandemic affected office vacancy rates and the commercial real estate sector?

The pandemic has led to a dramatic increase in office vacancy rates as companies adopted remote work policies, creating an oversupply of office space. This shift in demand has significantly contributed to the current commercial real estate crisis, with many properties now valued at much lower prices than before.

What impact does the commercial real estate crisis have on consumers?

The commercial real estate crisis can indirectly affect consumers through decreased pension fund values and tighter lending conditions, which may lead to lower consumer spending and less access to credit. Although the broader economy may remain stable, localized financial struggles can ripple through various sectors.

Will the commercial real estate crisis lead to a repeat of the 2008 financial crisis?

While the commercial real estate crisis poses significant risks, experts suggest it is unlikely to result in a crisis on the scale of 2008, primarily due to more stringent regulations on banks since then. However, localized impacts and bank failures could still pose serious challenges to financial stability.

What is the outlook for the commercial real estate sector moving forward?

The outlook for the commercial real estate sector is uncertain. If interest rates eventually stabilize or decrease, there may be opportunities for recovery. However, significant adjustments may still be needed, including potential bankruptcies and the need for innovative solutions to repurpose unused office spaces into viable properties.

| Key Point | Details |

|---|---|

| High Office Vacancy Rates | Vacancy rates in major U.S. cities range from 12% to 23%. Demand for downtown office spaces has decreased significantly since the pandemic. |

| Impact on Property Values | High vacancy rates are depressing property values, which is concerning for banks with significant investments in commercial real estate. |

| Commercial Mortgage Debt Maturity | 20% of the $4.7 trillion in commercial mortgage debt comes due this year, leading to worries of delinquencies. |

| Potential Bank Failures | Small and medium-sized banks may be more vulnerable due to less regulation, but big banks are better prepared to handle losses. |

| Factors Leading to Crisis | Over-leveraging and the pandemic’s impact on occupancy rates have created a difficult market for commercial real estate. |

| Broader Economic Concerns | While the commercial real estate sector is suffering, the overall economy remains solid with a strong job market and stock market. |

Summary

The commercial real estate crisis is a complex issue that poses significant challenges to the economy this year. Despite concerns over rising vacancy rates and the potential for bank failures, the overall economic outlook remains relatively stable. With prudent regulation in place and a recovering stock market, the situation is not as dire as the 2008 financial crisis. However, the risks associated with delinquent commercial real estate loans and their impact on smaller banks could create localized economic distress. Stakeholders are urged to monitor developments carefully as the situation evolves.