Corporate Tax Cuts: Analyzing the TCJA’s Impact

Corporate tax cuts have been a focal point of economic debate since the passage of the Tax Cuts and Jobs Act (TCJA) in 2017, igniting discussions on the implications of lowering corporate tax rates for businesses and the economy. As political powers gear up for a tax battle in 2025, the impact of these cuts on business investment growth remains a critical area of interest for policymakers and voters alike. An economic analysis by Harvard macroeconomist Gabriel Chodorow-Reich reveals not only modest increases in wages and investment but also significant challenges, including a stark decline in tax revenue. With the expiration of key provisions approaching, the TCJA’s effectiveness in driving growth and improving economic conditions is under intense scrutiny. Understanding the relationship between corporate tax cuts and overall economic health is essential, as stakeholders consider the long-term consequences of tax legislation on wealth distribution and public resources.

The discussion surrounding reductions in corporate taxation has sparked significant debate, particularly regarding the potential effects on the larger economic landscape. Terms like ‘business tax reductions’ and ‘corporate rate decreases’ are often used interchangeably in exploring how these changes influence capital flows and innovation. At the heart of this discourse lies the recent examination of the 2017 Tax Cuts and Jobs Act, which implemented notable changes to corporate tax policies aimed at stimulating economic growth. Analysts are now investigating whether these tax incentives have led to tangible improvements in business investment and job creation, or if they have simply resulted in diminished tax revenues for the government. As opinions on fiscal policy diverge, the conversation continues to evolve, stressing the need for informed perspectives on the future of corporate taxation.

Understanding the TCJA: Key Components and Their Impacts

The Tax Cuts and Jobs Act (TCJA), enacted in December 2017, aimed to overhaul the U.S. tax system significantly. One of its primary provisions included cutting the corporate tax rate from 35% to 21%, placing the U.S. in a competitive position relative to other wealthy nations. This legislative shift was largely driven by the belief that lower corporate tax rates would encourage business investment growth, ultimately spurring economic expansion. However, subsequent economic analyses have shown mixed results, with limited evidence supporting the idea that these cuts would pay for themselves through increased tax revenue.

Gabriel Chodorow-Reich and his co-authors conducted an in-depth examination of the TCJA’s real-world impacts, observing that while there was a notable rise in business investments—approximately 11%—the anticipated wage increases and overall economic benefits were less pronounced. The increase in capital investments did lead to some uptick in wages, but the figures fell significantly short of the projections made prior to the legislation. This discrepancy highlights the need for a more nuanced understanding of corporate tax cuts and their actual efficacy in stimulating the economy.

Corporate Tax Cuts: A Double-Edged Sword for Fiscal Policy

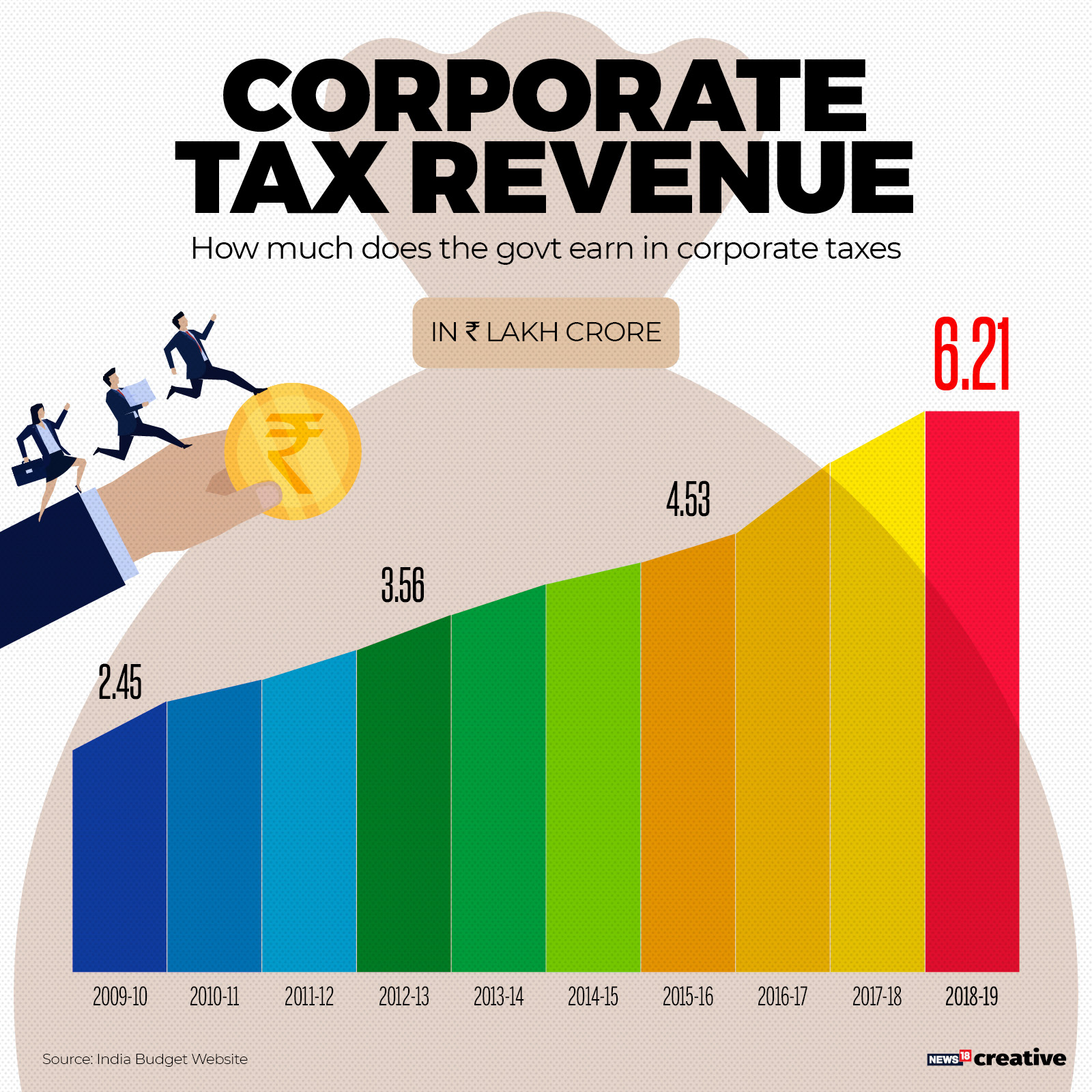

The debate surrounding corporate tax cuts often oscillates between two extremes: proponents argue that they stimulate job creation and economic growth, while opponents claim that they substantially reduce government tax revenue without delivering promised benefits. Chodorow-Reich’s analysis provides valuable insights, noting that although corporate tax revenue initially dropped by 40% after the TCJA’s implementation, it began to recover as business profits surged during the pandemic. This recovery suggests that while corporate tax cuts can lead to immediate revenue losses, they may create conditions that benefit government revenue in the long run, provided that other economic factors align favorably.

However, the complexity of the economic environment means that relying solely on corporate tax cuts to achieve fiscal stability is risky. The TCJA’s reductions were initially expected to generate greater tax revenues through increased investment and growth, yet evidence indicates that this has not materialized to the extent anticipated. As policymakers consider renewing or adjusting the TCJA’s provisions, carefully evaluating the balance between tax cuts and necessary tax revenues will be crucial to achieve sustainable economic growth without undermining public resources.

Economic Analysis of the TCJA’s Impact on Business Investments

One of the key focal points of the TCJA was the expectation that reduced corporate tax rates would incentivize businesses to invest more heavily in capital projects. Economic analysts, including Chodorow-Reich and his team, identified that the law indeed contributed to a significant uptick in business investment. The immediate expensing provisions enabled companies to write off the full cost of new investments, which proved to be a more effective driver of growth than statutory rate cuts alone. This suggests that targeted reforms focused on investment incentives could yield better returns on investment for the economy.

Nevertheless, the conversation does not end with the increase in investments. A deeper economic analysis reveals nuanced outcomes, such as wage growth that failed to meet initial expectations. Chodorow-Reich pointed out that while investments increased, the resultant wage growth was limited to an estimated $750 per full-time employee, starkly contrasting with predictions of increases ranging from $4,000 to $9,000. This divergence underscores the importance of scrutinizing the multifaceted relationship between tax policy and employment outcomes, as simplistic narratives about tax cuts frequently overlook core economic dynamics.

Corporate Tax Revenue Trends Post-TCJA: Recovery or Illusion?

Following the implementation of the TCJA, corporate tax revenue experienced a dramatic decline before starting to rebound in 2020. This resurgence has been interpreted in various ways—some experts view it as proof that corporate tax cuts can stimulate business profitability, while others caution against drawing definitive conclusions without comprehensive analysis. The rise in revenue post-2020 may not necessarily reflect the overall success of corporate tax cuts but could be attributed to external factors such as shifting global economic conditions and corporate behaviors influenced by the pandemic.

As the new electoral cycle unfolds, understanding the trajectory of corporate tax revenue will be crucial for policymakers. While the sharp decline in revenue following the TCJA raised alarms about future fiscal instability, the subsequent rebound raises questions about the sustainability of this recovery. Future economic analyses will need to account for variables like ‘greedflation’ and evolving international tax landscapes, which could significantly impact revenue projections and policy debates surrounding potential tax reforms.

The Political Ramifications of Corporate Tax Policy Debates

As Congress approaches significant tax battles, especially with key provisions of the TCJA set to expire, the political implications of corporate tax policy are becoming increasingly pronounced. Campaign speeches from figures such as Kamala Harris, advocating for higher corporate rates, juxtapose sharply with Donald Trump’s calls for further cuts. This polarized environment complicates the discourse surrounding corporate taxation, as parties leverage economic data selectively to support their ideological positions, often obscuring the intricacies of tax policy impacts on growth and revenue.

The political landscape also shapes public perception regarding corporate tax cuts and their effectiveness. With the elections on the horizon, voters will likely grapple with the contrasting narratives presented by political leaders. The challenge for elected officials will be to translate complex economic analyses, such as those conducted by Chodorow-Reich et al., into actionable policies that resonate with constituents. Achieving a balanced position that acknowledges the merits and drawbacks of tax cuts will be vital in crafting a tax policy that fosters sustainable economic growth while addressing critical funding needs.

Expiring Provisions: What Lies Ahead for Tax Policy?

As various provisions of the TCJA approach expiration in 2025, businesses and policymakers must prepare for potentially dramatic shifts in the tax landscape. Key measures, such as enhanced Child Tax Credits, have garnered significant public support, yet the fate of corporate tax cuts remains a focal point of contention. The upcoming discussions surrounding these expiring provisions could significantly reshape the business investment climate as lawmakers ponder whether to renew cuts on corporate rates or to reconsider their approach in light of recent economic data.

The decision-making process will require a careful balance between fostering business scalability and ensuring that government revenues remain robust enough to support public services. As past trends have shown, pulling back on the provisions that directly incentivized capital investments could impact future growth trajectories. Therefore, it is essential for Congress to analyze the ramifications thoroughly, employing an economic framework that prioritizes transparent and effective fiscal strategies that take into account the lessons learned from the TCJA.

The Role of Economic Analysis in Shaping Tax Policy

Economic analysis plays a pivotal role in informing tax policy decisions. As demonstrated by Chodorow-Reich’s thorough examination of the TCJA, the nuances of economic data can unveil deeper insights into the effects of tax policy on the overall economy. By analyzing corporate tax returns and macroeconomic trends, researchers establish a clearer picture of how corporate tax cuts influence investment behavior and, by extension, job creation and wage growth. This analytical framework is critical for developing future tax policies that align economic objectives with fiscal realities.

Moreover, the ongoing discourse around the TCJA emphasizes the need for policymakers to engage with robust economic analyses rather than rely on partisan rhetoric alone. Relevant studies provide the foundation for evidence-based policymaking, helping lawmakers frame tax reforms that may enhance business investments whiles ensuring fiscal responsibility. Engaging economic experts and actively incorporating their findings into legislative discussions will ultimately result in a more informed public debate around corporate taxation and its broader implications.

Balancing Growth and Revenue: Future of Corporate Tax Policy

The challenge of achieving a balance between fostering economic growth and ensuring adequate tax revenue continuously looms large in corporate tax policy discussions. With varying perspectives on the efficacy of corporate tax cuts, lawmakers face the daunting task of leveraging economic insights to navigate complex fiscal dilemmas. The TCJA serves as a case study for future taxation debates, as it highlights the intricacies involved in crafting policies that stimulate business investment while avoiding significant revenue shortfalls.

As Congress deliberates on corporate tax cuts going forward, new research is essential in guiding decisions that promote sustainable growth. Lawmakers may need to consider a mixed approach that includes maintaining competitive corporate tax rates while restructuring other provisions to incentivize business growth—such as reinstating effective expensing measures. Striking the right balance could pave the way for a more resilient economy, one that supports public services while adapting to the needs of an evolving business landscape.

The Long-Term Effects of Corporate Tax Cuts on American Economy

The long-term effects of corporate tax cuts enacted under the TCJA remain a critical area of inquiry among economists and policymakers alike. While short-term analysis reflects varying outcomes in terms of investment increases and wage growth, the sustainability of these benefits is paramount. Observing how the U.S. economy adapts to such changes post-TCJA will provide valuable lessons for future tax policy. Assessing whether corporate tax reductions can consistently drive economic performance without compromising revenue collection will undoubtedly lead to ongoing research in the field.

This longitudinal outlook is particularly relevant as businesses and lawmakers prepare for the potential expiration of TCJA provisions. Understanding the long-term implications of these cuts will inform future tax reforms amidst evolving global economic conditions. Policymakers must approach discussions surrounding corporate tax rates with a critical eye on historical data, developing policies that are not only responsive to current economic indicators but also forward-looking in ensuring the strength and resilience of the American economy.

Frequently Asked Questions

What are the effects of corporate tax cuts implemented by the TCJA on business investment growth?

The corporate tax cuts under the Tax Cuts and Jobs Act (TCJA) led to an increase in business investment, estimated at about 11%. By allowing companies to immediately write off capital expenses, the TCJA directly incentivized businesses to invest in new capital, showcasing that firms respond positively to changes in corporate tax policy.

How did the TCJA impact corporate tax rates and revenue?

The TCJA reduced the corporate tax rate from 35% to 21%, leading to an anticipated annual loss of federal corporate tax revenue of $100 billion to $150 billion over a decade. Initially, this caused a drastic 40% drop in corporate tax revenue, but it began to rebound by 2020 due to increased business profits.

What did economic analysis reveal about the impact of corporate tax cuts on wages?

Economic analysis conducted post-TCJA proposed that while the law would be expected to raise wages significantly, actual increases were modest. Estimates suggest that annual wage growth for full-time employees was closer to $750 rather than the $4,000 to $9,000 originally predicted, indicating that corporate tax cuts had limited immediate effects on wage growth.

What are some of the benefits and drawbacks of corporate tax cuts according to recent studies?

Recent studies highlight that while corporate tax cuts under the TCJA had some benefits, such as increased business investment and modest wage growth, the drawbacks included a significant shortfall in tax revenue. The cuts did not fully pay for themselves through the anticipated higher business activity, challenging the belief that lower corporate tax rates would lead to substantial economic benefits.

What might happen to corporate tax cuts in future legislation, given the current political climate?

With key provisions of the TCJA nearing expiration in 2025, future legislation may see both sides of the political spectrum arguing for adjustments. Democrats, like Kamala Harris, advocate for increased corporate tax rates to facilitate funding for other initiatives, while Republicans, including Donald Trump, may push for further cuts to encourage growth, indicating a contentious debate ahead.

| Key Aspect | Details |

|---|---|

| Background | The 2017 Tax Cuts and Jobs Act (TCJA) significantly altered corporate tax rates, cutting them from 35% to 21%. |

| Impacts on Revenue | The TCJA projected a reduction in federal corporate tax revenue by approximately $100 billion to $150 billion annually over a decade. |

| Effects on Investment | The law led to an estimated 11% increase in capital investments but results were mixed and fell short of expectations. |

| Wage Effects | There was a modest wage increase of around $750 annually per full-time employee, significantly lower than initial projections. |

| Future Implications | As parts of the TCJA are set to expire, lawmakers face decisions on renewing corporate tax cuts versus increasing rates. |

Summary

Corporate tax cuts have been a polarizing topic in American politics, especially following the enactment of the 2017 Tax Cuts and Jobs Act. This legislation aimed to reduce tax rates for corporations substantially, influencing investment behaviors and tax revenues. However, while there were increases in capital investments, the gains did not equate to a balanced offset for the revenue losses experienced by the federal government. As key provisions are poised to expire, the dialogue surrounding corporate tax cuts has shifted towards whether to retain these reductions or reconsider tax structures for improved revenue generation going forward.